14 Gradient Boosting Machines

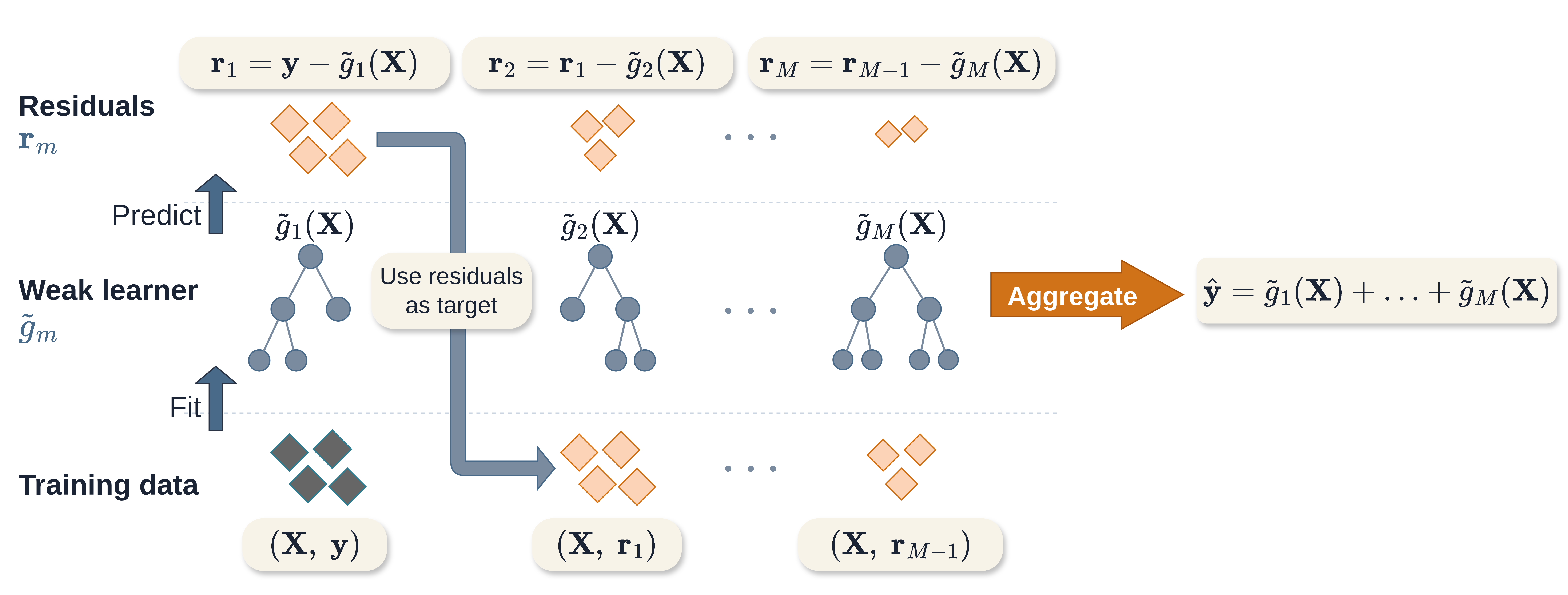

Similarly to random forests, boosting is an ensemble method that creates a powerful model from a combination of weak learners that make poor predictions individually. However, the two methods differ in how individual learners are selected and combined: in random forests, each decision tree is grown independently and predictions are averaged. In boosting, weak learners are fit sequentially with errors from one learner used to train the next, and predictions are made by a weighted linear combination of all learners (Figure 14.1).

14.1 GBMs for regression

Gradient boosting machines (GBMs) are among the most widely used families of boosting algorithms. The general idea, inspired by gradient descent (Section 2.6.1), is to choose a differentiable loss function and iteratively improve predictions by fitting weak learners to the remaining errors from the current model. These errors correspond to the negative gradients, or pseudo-residuals. Figure 14.1 illustrates this process in a least-squares regression setting, where the negative gradient corresponds to the ordinary residual, which is the observed outcome minus the current prediction. This procedure can be understood as follows:

- An initial, simple model is fit to the data to obtain the first set of predictions.

- The errors of this model are computed by comparing predictions to the observed outcomes.

- A weak learner is fit to these errors, focusing on patterns that the previous model failed to capture.

- The new learner is added to the existing model, improving the overall prediction.

- This is repeated with each learner correcting the errors of the current model.

Predictions are therefore built up gradually as a sum of many weak learners, each making a small contribution to the final model.

Practically, a number of important hyperparameters are used to control and optimize the algorithm while reducing overfitting. These are:

Number of iterations, \(M\): The number of iterations is often claimed to be the most important hyperparameter in GBMs and it has been demonstrated that a value too small will result in underfitting, while a value too large will result in overfitting (Buhlmann 2006; Hastie et al. 2001; Schmid and Hothorn 2008a). This underlines the general idea of boosting weak learners to slowly construct a single powerful model.

Step size, \(\alpha\): The step size parameter is a shrinkage parameter that controls the contribution of the weak learner at each iteration. Several studies have demonstrated that GBMs perform better when shrinkage is applied and a value of \(\alpha \leq 0.1\) is often suggested (Buhlmann and Hothorn 2007; Friedman 2001; Hastie et al. 2001; Lee et al. 2021; Schmid and Hothorn 2008a). The optimal values of \(\alpha\) and \(M\) depend on each other, such that smaller values of \(\alpha\) require larger values of \(M\), and vice versa. This is intuitive as smaller \(\alpha\) results in slower learning and therefore more iterations are required to fit the model. A practical procedure is to set \(\alpha\) to a small value (such as \(0.1\)) and \(M\) to a very large value (such as \(10,\!000\)), then use early stopping (Section 2.6.2) to halt the algorithm once performance on a validation set stops improving. This avoids the need for computationally expensive tuning to find the optimal combination of \(\alpha\) and \(M\).

Subsampling proportion, \(\phi\): Sampling a fraction, \(\phi\), of the training data at each iteration can improve performance and reduce runtime (Hastie et al. 2001), with \(\phi = 0.5\) often used although ideally it should be tuned. Motivated by the success of bagging in random forests, stochastic gradient boosting (Friedman 1999) randomly samples the data in each iteration. Subsampling appears to perform best when combined with shrinkage (Hastie et al. 2001).

In addition to these parameters, the hyperparameters of the underlying weak learner are also commonly tuned. When using decision trees, it is usual to restrict the number of terminal nodes in the tree to be between four and eight, corresponding to shallow trees with limited interaction depth. With these hyperparameters and some differentiable loss \(L\), the general gradient boosting machine algorithm is given in Algorithm 2.

Once the model is trained, predictions are made for new data, \(\mathbf{x}_*\) with:

\[ \hat{g}_M(\mathbf{x}_*) = \hat{g}_0 + \alpha \sum^M_{m=1} \tilde{g}_m(\mathbf{x}_*). \]

GBMs provide a flexible, modular algorithm, primarily composed of a differentiable loss to minimize, \(L\), and the selection of weak learners. Perhaps the most common weak learners are decision trees, linear least squares (Friedman 2001) and smoothing splines (Bühlmann and Yu 2003). Trees allow the structure of the resulting prediction function to vary substantially; for example, using stumps (trees with only one split) results in an additive model with main effects only, whereas decision trees with an extra layer yield two-way interactions.

14.2 GBMs for survival analysis

Unlike other model classes, survival analysis was considered in early GBM papers (Ridgeway 1999), although there appears to have been a decade-long gap before further advances were made. Subsequently, Hothorn et al. (2005), Schmid and Hothorn (2008b), Schmid and Hothorn (2008a), and Binder and Schumacher (2008) further developed GBM frameworks for survival analysis, which are discussed in this chapter.

In principle, boosting could be applied to models that directly predict a full survival distribution by optimizing a proper scoring rule (Chapter 8). However, standard boosting updates a single real-valued function at each iteration by fitting to the residual errors. When the target is a full survival distribution, scoring rules aggregate prediction errors across time, making it difficult to attribute errors to specific regions of the prediction and construct effective updates. This may partly explain why boosting methods in survival analysis are often applied to models that produce scalar risk scores.

This section begins with boosting approaches based on the core models introduced in Chapter 11, specifically proportional hazards (PH) and accelerated failure time (AFT) models (Section 14.2.1). In the case of the AFT models, the model parameters are estimated directly, which specifies a full survival distribution prediction. The discussion then extends to approaches that do not assume a specific model form, but instead directly optimize discriminatory ability by using a concordance index (Chapter 6) as the loss (Section 14.2.2).

14.2.1 Likelihood boosting

The negative log-likelihood of the semi-parametric PH and fully-parametric AFT models can be derived from the (partial) likelihoods presented in Section 11.2.2 and Section 11.3 respectively.

14.2.1.1 Cox proportional hazards boosting

To boost a Cox-type model, at each iteration, the weak learner in Algorithm 2 is taken to be a linear predictor,

\[ g_m(\mathbf{x}_i) = \eta_{m;i} = \mathbf{x}_i^\top\boldsymbol{\beta}_m, \tag{14.1}\]

where \(\eta_{m;i}\) is the updated linear predictor in iteration \(m\) and \(\eta_{0;i} = 0\).

Recall the Cox partial likelihood (11.7) given by (Cox 1972, 1975),

\[ \mathcal{L}_{PL}(\boldsymbol{\beta}) = \prod_{k=1}^{\tilde{n}} \left(\frac{\exp(\eta_{i_{(k)}})}{\sum_{j \in \mathcal{R}_{t_{(k)}}} \exp(\eta_j)}\right), \]

with corresponding negative log-likelihood (11.8):

\[ -\ell_{PL}(\boldsymbol{\beta}) = -\sum_{k=1}^{\tilde{n}} \left(\eta_{i_{(k)}} - \log \left(\sum_{j \in \mathcal{R}_{t_{(k)}}} \exp(\eta_j)\right)\right), \tag{14.2}\]

where \(t_{(k)}\) is the \(k\)th ordered event time for \(\tilde{n} < n\) event times, \(\mathcal{R}_{t_{(k)}}\) is the set of patients at risk at time \(t_{(k)}\) (assuming no ties).

The negative gradient of \(-\ell_{PL}(\boldsymbol{\beta})\) at iteration \(m\) is then given by substituting (14.1) for \(\eta_i\) into the negative log-likelihood (14.2) and differentiating (Ridgeway 1999):

\[ r_{im} := \delta_i - \sum^{\tilde{n}}_{k=1} \frac{\mathbb{I}(t_i \geq t_{(k)}) \exp(\hat{g}_{m-1}(\mathbf{x}_i))}{\sum_{j \in \mathcal{R}_{t_{(k)}}} \exp(\hat{g}_{m-1}(\mathbf{x}_j))}. \]

14.2.1.2 Accelerated failure time boosting

For non-PH data, boosting an AFT model can outperform boosted PH models (Schmid and Hothorn 2008b). Recall from Section 11.3 the log-linear AFT model (11.23) defined by:

\[ \log(t_i) = \mu + \eta_i + \sigma\epsilon_i, \]

where \(\sigma\) is a scale parameter, \(\epsilon_i\) is an error term, and \(\mu\) is an intercept. The model is now boosted by updating

\[ \hat{g}_m(\mathbf{x}_i) = \mu + \eta_i, \]

and then estimating \(\hat{\sigma}_m\) using the updated \(\hat{g}_m\); usually \(\sigma_0 = 1\) (Schmid and Hothorn 2008b). Rearranging (11.23) in terms of \(\epsilon_i\) and \(\hat{g}\) gives,

\[ \epsilon_i = \frac{\log(t_i) - \hat{g}_m(\mathbf{x}_i)}{\sigma}. \tag{14.3}\]

By assuming a distribution on \(\epsilon_i\), a distribution is assumed for the full parametric distribution of the survival time, giving the AFT log-likelihood (Klein and Moeschberger 2003),

\[ \begin{aligned} -\ell^{AFT}(g, \sigma) & = -\sum^n_{i=1} \Bigg[ \delta_i\Bigg(- \log{\sigma} + \log f_{\epsilon}\Big(\frac{\log(t_i) - g(\mathbf{x}_i)}{\sigma}\Big)\Bigg) \\ & + (1-\delta_i)\Bigg(\log S_{\epsilon}\Big(\frac{\log(t_i) - g(\mathbf{x}_i)}{\sigma}\Big)\Bigg) \Bigg] \end{aligned}, \tag{14.4}\]

where \(f_{\epsilon}, S_{\epsilon}\) are the density and survival functions of \(\epsilon\) respectively assuming a shared error distribution for all observations, and the expressions within \(f_{\epsilon}\) and \(S_{\epsilon}\) are a substitution of the error term (14.3). At iteration \(m\), (14.4) is evaluated at \((\hat{g}_{m-1}, \hat{\sigma}_{m-1})\) to compute the pseudo-residuals used to update \(\hat{g}_m\) following Algorithm 2,

\[ r_{im} = -\frac{\partial(-\ell^{AFT}(\hat{g}_{m-1}, \hat{\sigma}_{m-1}))}{\partial \hat{g}_{m-1}(\mathbf{x}_i)}. \]

The only change to the algorithm is a final step in each iteration where the scale parameter is re-estimated conditional on the updated \(\hat{g}_m\), by minimizing (14.4) with respect to \(\sigma\):

\[ \hat{\sigma}_m := \mathop{\mathrm{arg\,min}}_{\sigma > 0} \ -\ell^{AFT}(\hat{g}_m, \sigma), \]

which is the conditional maximum likelihood estimate of \(\sigma\) given the current boosted fit and is usually obtained by a one-dimensional numerical optimization over \(\sigma > 0\).

As well as boosting fully-parametric AFTs, one could consider boosting semi-parametric AFTs, for example, with the Gehan loss (Johnson and Long 2011) or using Buckley-James imputation (Wang and Wang 2010). However, known problems with semi-parametric AFT models and the Buckley-James procedure (Wei 1992), as well as a lack of off-the-shelf implementation, mean that these methods appear to be rarely used in practice.

The flexibility of boosting allows extensions to other censoring and truncation types to follow simply by replacing the likelihood functions above with the corresponding objective functions in Section 3.5.1.

14.2.1.3 Penalized boosting

‘CoxBoost’ (Binder and Schumacher 2008) is an alternative method to boost Cox models and has been demonstrated to perform well in experiments (Burk et al. 2026). The algorithm can be interpreted as a componentwise boosting procedure for Cox models, where at each iteration a single covariate is selected, alongside mandatory (or ‘forced’) covariates, and coefficients are updated using a penalized second-order optimization step (Binder and Schumacher 2008). In medical domains the inclusion of mandatory covariates may be essential, either for model interpretability, or due to prior expert knowledge. CoxBoost deviates from Algorithm 2 by instead using an offset-based approach for generalized linear models (Tutz and Binder 2007).

As this method is more technically involved than standard gradient boosting, consider the following motivational example (Table 14.1). Suppose treatment group is considered clinically essential and must always be included in the model, while age and a biomarker are optional covariates. In each boosting iteration, CoxBoost considers candidate updates componentwise by adding one optional covariate at a time to the mandatory covariate. In this example, the two candidate updates are therefore treatment group with age or treatment group with the biomarker. At each iteration, the candidate update with the lower loss (in bold) is selected and added to the coefficient vector. For example, in iteration \(1\), the update using age gives a lower loss than the update using the biomarker, so the coefficients for treatment group and age are updated. In iteration \(2\), the update using the biomarker gives a lower loss, so the coefficients for treatment group and the biomarker are updated instead. The optional covariate that is not selected in a given iteration is left unchanged. The running coefficient vector \(\hat{\boldsymbol{\beta}}_m\) plays the same role as the cumulative boosted predictor \(\hat{g}_m\) in Algorithm 2. The vector \(\hat{\boldsymbol{\gamma}}_{mk}\) is the candidate increment being considered in iteration \(m\) for candidate set \(k\). For the selected candidate \(k^*\), \(\hat{\boldsymbol{\gamma}}_{mk^*}\) is added to \(\hat{\boldsymbol{\beta}}_{m-1}\) to obtain \(\hat{\boldsymbol{\beta}}_m\), analogous to adding the new learner contribution \(\alpha \tilde{g}_m\) in standard gradient boosting.

| \(m\) | Candidate covariate | Loss after update | \(\hat{\gamma}_{mk^*,\text{trt}}\) | \(\hat{\gamma}_{mk^*,\text{opt}}\) | \(\hat{\beta}_{m,\text{trt}}\) | \(\hat{\beta}_{m,\text{age}}\) | \(\hat{\beta}_{m,\text{bio}}\) |

|---|---|---|---|---|---|---|---|

| 0 | – | – | – | – | 0.00 | 0.00 | 0.00 |

| 1 | Age | 1.42 | 0.08 | 0.15 | 0.08 | 0.15 | 0.00 |

| 1 | Biomarker | 1.55 | – | – | 0.08 | 0.15 | 0.00 |

| 2 | Age | 1.31 | – | – | 0.08 | 0.15 | 0.00 |

| 2 | Biomarker | 1.20 | 0.03 | 0.20 | 0.11 | 0.15 | 0.20 |

| 3 | Age | 1.11 | -0.02 | 0.06 | 0.09 | 0.21 | 0.20 |

| 3 | Biomarker | 1.18 | – | – | 0.09 | 0.21 | 0.20 |

After the final iteration in Table 14.1, the fitted model for observation \(i\) is therefore

\[ \hat{h}(\tau \mid \mathbf{x}_i) = \hat{h}_0(\tau)\exp(0.09x_{i,\mathrm{trt}} + 0.21x_{i,\mathrm{age}} + 0.20x_{i,\mathrm{bio}}), \]

where the coefficients are the final accumulated values in \(\hat{\boldsymbol{\beta}}_3\).

To formally introduce the model, let \(\mathcal{I}= \{1,\ldots,p\}\) be the indices of the covariates, let \(\mathcal{I}_{\text{mand}}\) be the indices of the mandatory covariates that must be included in all iterations, and let \(\mathcal{I}_{\text{opt}} = \mathcal{I}\setminus \mathcal{I}_{\text{mand}}\) be the indices of the optional covariates that may be included in any iteration. In each iteration, the algorithm considers models that include all mandatory covariates together with a single optional covariate, selecting the covariate that yields the greatest improvement in the penalized likelihood:

\[ \mathcal{I}_{mk} = \mathcal{I}_{\text{mand}} \cup \{k\}, \quad k \in \mathcal{I}_{\text{opt}}. \]

In addition, a penalty matrix \(\mathbf{P} \in \mathbb{R}^{p \times p}\) is considered such that \(P_{ii} > 0\) implies that covariate \(i\) is penalized and \(P_{ii} = 0\) means no penalization. In practice, this is usually a diagonal matrix (Binder and Schumacher 2008) and by setting \(P_{ii} = 0, i \in \mathcal{I}_{\text{mand}}\) and \(P_{ii} > 0, i \not\in \mathcal{I}_{\text{mand}}\), only optional (non-mandatory) covariates are penalized. The penalty matrix can vary with each iteration, which allows for a highly flexible approach. In practice, a simpler approach is to use the same penalty matrix in each iteration and to apply the same penalty factor to all penalized covariates (Binder 2013).

At the \(m\)th iteration and the \(k\)th set of indices to consider, the penalized partial log-likelihood is given by,

\[ \begin{aligned} &l_{pen}(\boldsymbol{\gamma}_{mk}) = \\ &\sum_{\tau=1}^{\tilde{n}} \left[\eta_{i_{(\tau)},m-1} + \mathbf{x}_{i_{(\tau)},\mathcal{I}_{mk}}^\top\boldsymbol{\gamma}_{mk} - \log\left(\sum_{j \in \mathcal{R}_{t_{(\tau)}}} \exp\left(\eta_{j,m-1} + \mathbf{x}_{j,\mathcal{I}_{mk}}^\top\boldsymbol{\gamma}_{mk}\right)\right)\right] - \lambda\boldsymbol{\gamma}^\top_{mk}\mathbf{P}\boldsymbol{\gamma}_{mk}. \end{aligned} \tag{14.5}\]

where \(\eta_{i,m} = \mathbf{x}_i^\top\boldsymbol{\beta}_m\), \(\boldsymbol{\gamma}_{mk}\) are the coefficient updates corresponding to the candidate covariate set \(\mathcal{I}_{mk}\), \(\mathbf{P}\) is the penalty matrix (assuming the same in every iteration), \(\lambda\) is a penalty hyperparameter, and \(t_{(\tau)}\) is the \(\tau\)th ordered event time for \(\tilde{n} < n\) unique event times (assuming no ties).

In each iteration, all potential candidate sets are considered and the optimal set is the one that results in the largest improvement in the penalized partial log-likelihood. Note that CoxBoost uses Fisher scoring iterations to update the coefficient estimates, using both first and second derivatives, whereas standard GBMs only use first derivatives.

The optimal set is then found as,

\[ k^* := \mathop{\mathrm{arg\,max}}_k \ l_{pen}(\hat{\boldsymbol{\gamma}}_{mk}), \]

and the estimated coefficients are updated by,

\[ \hat{\beta}_{m, j} = \begin{cases} \hat{\beta}_{m-1, j} + \hat{\gamma}_{mk^*,j}, & j \in \mathcal{I}_{mk^*}, \\ \hat{\beta}_{m-1, j}, & j \notin \mathcal{I}_{mk^*}, \end{cases} \quad j = 1, \ldots, p, \]

where \(\hat{\gamma}_{mk^*,j}\) is the \(j\)th element in \(\hat{\boldsymbol{\gamma}}_{mk^*}\). In words, \(\hat{\boldsymbol{\beta}}_m\) is the cumulative coefficient vector after iteration \(m\), while \(\hat{\boldsymbol{\gamma}}_{mk^*}\) is the selected increment at that iteration. Thus CoxBoost updates the fitted linear predictor by adding the selected coefficient increment, analogous to adding a new weak learner in standard gradient boosting. At iteration \(m\), the components of \(\hat{\boldsymbol{\beta}}\) in the optimal set \(\mathcal{I}_{mk^*}\) are increased by \(\hat{\boldsymbol{\gamma}}_{mk^*}\), while all other components remain unchanged.

CoxBoost is extended to the competing risks setting by boosting a subdistribution PH model (Binder et al. 2009). In this setting, (14.5) is replaced by the log-likelihood from the Fine and Gray model (Section 11.2.3) with an analogous penalty function, and the remaining steps proceed similarly.

14.2.2 Measure-based boosting

Instead of optimizing a likelihood tied to a specific model form, such as a PH or AFT model, boosting can also directly optimize an evaluation measure (Part II). Common choices are discrimination measures, such as Uno’s or Harrell’s C (Chen et al. 2013; Mayr and Schmid 2014).

Consider Uno’s C (Section 6.1), which at iteration \(m\) is evaluated using the prediction from the previous iteration, \(\hat{g}_{m-1}\):

\[ \begin{aligned} &C_U(\hat{g}_{m-1}, \mathbf{X}, \mathbf{t}, \boldsymbol{\delta}\mid \tau) =\\ &\quad\frac {\sum_{i\neq j} \delta_i(\hat{G}_{KM}(t_i))^{-2}\mathbb{I}(t_i < t_j, t_i < \tau)\mathbb{I}(\hat{g}_{m-1}(\mathbf{x}_i) > \hat{g}_{m-1}(\mathbf{x}_j))} {\sum_{i\neq j}\delta_i(\hat{G}_{KM}(t_i))^{-2}\mathbb{I}(t_i < t_j, t_i < \tau)}, \end{aligned} \tag{14.6}\]

where \(\hat{G}_{KM}\) is the Kaplan-Meier estimate of the censoring distribution.

The GBM algorithm requires that the optimized objective be differentiable with respect to \(\hat{g}(\mathbf{x})\). However, the indicator term is not differentiable with respect to the prediction scores. The measure can be made differentiable by replacing the indicator with a logistic sigmoid function (Ma and Huang 2006):

\[ K(x, y \mid \omega) = \frac{1}{1 + \exp((y - x)/\omega)}, \tag{14.7}\]

where \(\omega\) is a tunable hyperparameter controlling the smoothness of the approximation. Smaller values of \(\omega\) produce a closer approximation to the indicator function but may lead to unstable gradients, whereas larger values yield smoother gradients at the cost of a poorer approximation to the indicator function.

Replacing \(\mathbb{I}(\hat{g}_{m-1}(\mathbf{x}_i) > \hat{g}_{m-1}(\mathbf{x}_j))\) in (14.6) with (14.7) yields the smooth objective to optimize,

\[ \begin{aligned} &C_{\tilde{U}}(\hat{g}_{m-1}, \mathbf{X}, \mathbf{t}, \boldsymbol{\delta}\mid \omega, \tau) =\\ &\quad\frac{\sum_{i \neq j} \delta_i (\hat{G}_{KM}(t_i))^{-2}\mathbb{I}(t_i < t_j, t_i < \tau)K(\hat{g}_{m-1}(\mathbf{x}_i), \hat{g}_{m-1}(\mathbf{x}_j) \mid \omega)} {\sum_{i \ne j} \delta_i (\hat{G}_{KM}(t_i))^{-2}\mathbb{I}(t_i < t_j, t_i < \tau)}. \end{aligned} \tag{14.8}\]

The GBM algorithm is then followed as normal with the negative smoothed C-index (14.8) and its gradient. One advantage of this method is that it may be relatively insensitive to overfitting, meaning discrimination performance can remain stable even with many boosting iterations (Mayr et al. 2016).

Similarly to likelihood boosting, flexibility is again a key advantage here for extensions to other censoring and truncation types and also to competing risks. For example, the all-cause logarithmic score (Section 8.5) can be used to boost survival models by optimizing overall predictive performance across all competing event types (Alberge et al. 2025).